When listening to the news media reporting on U.S. housing market trends, it is easy to confuse claims of the market being “up” or “down” to mean that the entire U.S. is just one big real estate market. The reality is that there are thousands of different fragmented real estate markets in the U.S., each with different drivers that affect prices in those areas. When analyzing the different demand drivers and trends of these diverse real estate markets across the country, they can largely be broken down into three different types of markets: cyclical, linear, and hybrid. Cyclical markets refer to markets that have a lot of volatility and sometimes wild swings in home prices – markets like San Francisco, Los Angeles, Miami, and New York. Linear markets, on the other hand, have historically had much more steady growth, without dramatic increases in prices, but also without dramatic decreases in prices – markets like Memphis, Columbus, Birmingham, and Little Rock. Hybrid markets are a combination of the two – markets like Denver or Phoenix.

The financial crisis of 2008-2010 provides the exhibit to showcase the effect that economic stress puts on housing prices in these different types of markets. Since we now how the luxury of looking back on this tumultuous time to help guide our investment strategy during the Covid era, it is worth looking at some hard data. The Case-Shiller Index, as published by the Federal Reserve Bank of St. Louis, is widely regarded as the foremost authority in tracking U.S. home prices.

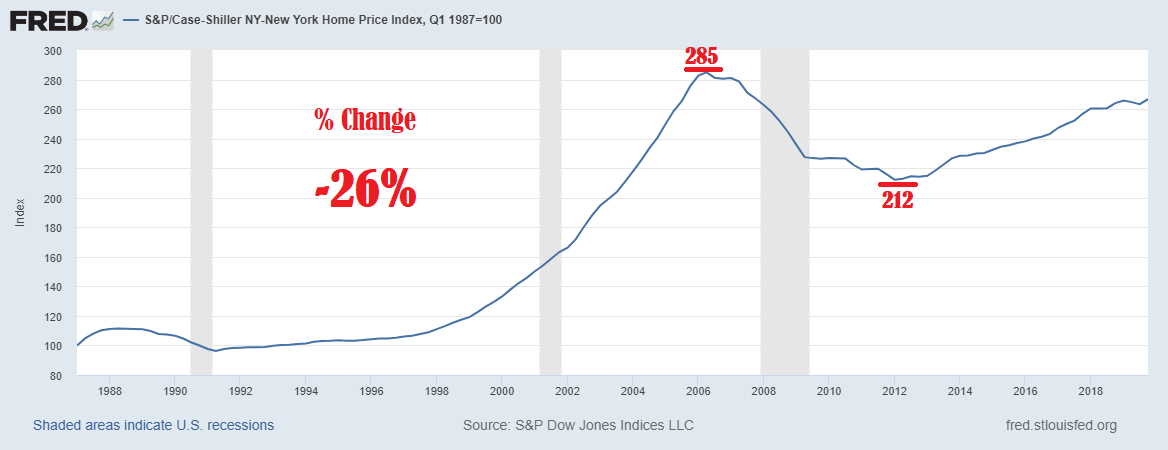

We’ve taken data sets from the Case Shiller Index showing prices from Q1 1987 to Q4 2019, with Q1 1987 setting the index base at 100. The index high before the financial crisis, as well as the index low at the end of the financial crisis, are highlighted and used to calculate a percentage change during that period.

First, let’s start with the cyclical markets of San Francisco, Los Angeles, Miami, and New York:

SAN FRANCISCO

LOS ANGELES

MIAMI

NEW YORK CITY

As we can see, the changes in these markets during the financial crisis were quite dramatic. How does this compare to the U.S. as a whole?

UNITED STATES

If the price decrease was so dramatic in some of the largest real estate markets in the U.S., then why is it that the average decline in U.S. real estate prices was not nearly as severe (only 19% compared to 40-50% in some markets). The answer is that the linear markets provided relative stability during these chaotic times. Sure, they also experienced a decrease, but not nearly as severe. We’d like to highlight Memphis, as it is one of our strongest markets and one that we’ve had a lot of success investing in, even in the wake of the financial crisis.

MEMPHIS

As we can see, Memphis weathered the storm quite vigilantly. What’s more, because prices did not dip so severely during the financial crisis, prices in Memphis have now greatly exceeded their pre-financial crisis highs, whereas prices in New York and Miami still have not fully recovered. Looking back even further, we can also see volatility in prices in San Francisco, Los Angeles, and New York City in the wake of the 1987 recession, whereas Memphis saw steady growth all the way through until the Great Recession started to take hold in 2007.

It’s impossible to time the market, so it’s best to take price fluctuations out of the equation. Every deal should deliver positive cash flow from day one, and not bank on appreciation in order to make it work. If the goal is to build up a strong portfolio of cash flowing assets, then the actual market value of the property at any given time is much less significant, especially if those assets will be held onto long term. As we’ve seen in the chart above for Memphis, it is very reasonable to expect that prices will steadily increase in good times, and that the down side will be well protected in down times. If you’re collecting rental income every month from your cash flowing properties, any appreciation will just be icing on the cake.

DATA SOURCE: S&P Dow Jones Indices LLC, S&P/Case-Shiller 20-City Composite Home Price Index [SPCS20RSA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/SPCS20RSA, April 19, 2020.